Mortgage Rates Today: The Real Data & Its Implications

Mortgage Rates Dance Around 6%: Is This the New Normal?

The 6% Tango

Mortgage rates are doing a little dance around the 6% mark. Zillow is reporting an average 30-year fixed rate of 6.06%, tying the lowest rate we've seen so far in 2025. (Remember when everyone was freaking out about 7%? Good times.) This figure is mirrored by other sources, though there are some discrepancies depending on the data aggregator. Optimal Blue, for instance, has the 30-year fixed at 6.224%. A minor difference, but it highlights the importance of looking at multiple data points. Mortgage and refinance interest rates today, November 25, 2025: Lowest 30-year rate this year

The spread between the 30-year and 15-year fixed is holding steady, with the 15-year hovering around 5.5%. This is where the math starts to get interesting. A $400,000 mortgage at 6.06% over 30 years will cost you roughly $468,915 in interest. Cut that term in half at 5.53%, and you're looking at $189,447 in interest. That's a difference of nearly $280,000. The catch, of course, is that your monthly payments jump from around $2,414 to $3,275. Ouch.

The adjustable-rate mortgage (ARM) is still hanging around, but it's not looking particularly attractive. A 5/1 ARM is averaging around 6.16%. The supposed benefit of an ARM is a lower initial rate. However, with fixed rates already in the low 6% range, the incentive to gamble on future rate hikes has diminished significantly.

Decoding the Fed's Next Move

Economists aren't expecting any drastic drops in mortgage rates before the end of the year. The Federal Reserve has already cut rates twice in 2025, including one at its most recent meeting in October. The CME FedWatch tool is currently predicting an 85% chance of another quarter-point cut at the December meeting.

But here's where my skepticism kicks in. Those FedWatch probabilities are based on futures contracts, which are essentially bets on what the Fed will do. And those bets are often wrong. Remember back in 2024 when the market was pricing in multiple rate increases that never materialized?

The article also mentions that the Fed decreased its rate again at its November and December meetings (by 25 bps each time). However, it paused for months to consider the next move.

So, while another rate cut is certainly possible, it's far from a sure thing. And even if it does happen, a quarter-point cut is unlikely to send mortgage rates plummeting. We're more likely to see a slow, grinding decline over time, rather than a sudden drop.

The Real Cost of Waiting

So, is 6% the new normal? It's certainly starting to feel that way. The market seems to have priced in the Fed's rate cuts, and we're unlikely to see a return to the rock-bottom rates of the pandemic era anytime soon.

Waiting for rates to drop further is a gamble. You might save a few basis points, but you also risk missing out on potential home price appreciation. And let's not forget the opportunity cost of renting. Every month you spend renting is money you're not putting towards building equity.

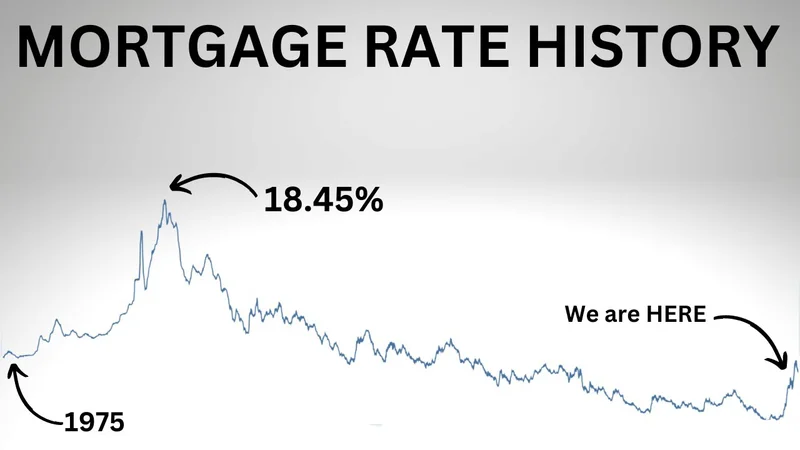

Ultimately, the decision to buy or refinance depends on your individual circumstances. But if you're on the fence, it's worth running the numbers and seeing if a 6% rate makes sense for you. It might not be the dream rate you were hoping for, but it's a far cry from the double-digit rates of the 1980s.

Don't Bet on a Miracle

The data suggests we're in for a period of relative stability in mortgage rates. Waiting for a dramatic drop is likely to be a losing game. The new normal is here, and it's time to adjust our expectations accordingly.

-

Warren Buffett's OXY Stock Play: The Latest Drama, Buffett's Angle, and Why You Shouldn't Believe the Hype

Solet'sgetthisstraight.Occide...

-

The Great Up-Leveling: What's Happening Now and How We Step Up

Haveyoueverfeltlikeyou'redri...

-

The Future of Auto Parts: How to Find Any Part Instantly and What Comes Next

Walkintoany`autoparts`store—a...

-

Applied Digital (APLD) Stock: Analyzing the Surge, Analyst Targets, and Its Real Valuation

AppliedDigital'sParabolicRise:...

-

Analyzing Robinhood: What the New Gold Card Means for its 2025 Stock Price

Robinhood's$123BillionBet:IsT...

- Search

- Recently Published

-

- Ethereum ETFs Surge: Who's Profiting From the Plunge? - Redditors Are Shook

- Niklas Freihofer's Sales Strategy Leadership: What His Fintech & Brokerage Expertise Actually Means

- Why Crypto Analysis is Just BS - Crypto Talk Heats Up

- Why AI in Trading is Revolutionizing Wealth - Traders in Shambles

- Pi Network: Price, Updates, and the Data-Driven Reality

- Alibaba Stock: The Price Today & Why You Still Can't Trust the 'Experts'

- NASA's Interstellar Comet 3I/ATLAS: Unlocking Its Secrets and Our Cosmic Future

- Irys: That 'Revolutionary' Listing and the Fake Contract Debacle

- Childcare: The Promise of Universal and Free Access

- Mortgage Rates Today: The Real Data & Its Implications

- Tag list

-

- Blockchain (11)

- Decentralization (5)

- Cryptocurrency (26)

- DeFi (5)

- Bitcoin (31)

- Trump (5)

- Ethereum (8)

- Pudgy Penguins (6)

- NFT (5)

- Solana (5)

- cryptocurrency (6)

- bitcoin (7)

- Plasma (5)

- Zcash (12)

- Aster (10)

- nbis stock (5)

- iren stock (5)

- crypto (7)

- ZKsync (5)

- irs stimulus checks 2025 (6)

- pi (6)

- hims stock (5)

- kimberly clark (5)

- uae (5)

- uber stock (5)